…a little with the head of Maradona, and a little with the hand of God

Diego Maradona, 22nd June 1986, at the World Cup, Mexico

It seems like yesterday. That burning feeling of injustice as Argentinian Diego Maradona (5ft 5in) managed to out-leap Peter Shilton (6ft) to put the ball in the back of the net. Although hard to see exactly what had happened, the reaction from the players said it all. We subsequently learned that he used his hand to score. The result was yet another ignominious ejection of England from the World Cup. I remember watching it at school with friends in what was known as the library (which was notable for the fact that it contained not a single book) and can picture the moment to this day.

But it is not this goal scored by the golden boy that we wish to remember. Rather it is the remarkable solo effort in the same match that saw him execute a brilliant turn before taking off with the ball, running half the length of the pitch and scoring. It is considered by some to be the greatest individual goal ever scored in the World Cup.

What is also thought to be remarkable was the way he did it. I quote none other than Mervyn King, Governor of the Bank of England in his Mais Lecture “Monetary Policy: Practice Ahead of Theory” on 17th May 2005 at Cass Business School in London.

“Maradona ran 60 yards from inside his own half beating five players before placing the ball in the English goal. The truly remarkable thing, however, is that Maradona ran virtually in a straight line. How can you beat five players by running in a straight line? The answer is that the English defenders reacted to what they expected Maradona to do. Because they expected Maradona to move either left or right, he was able to go straight on.”

The Governor was making a point about market reactions to expected monetary policy. I wish to use the Maradona example to make a different point – that the economic outlook is uncertain and the US equity market is very fully valued and we should see this for precisely what it is and maintain our cautious stance.

Priced for perfection

The US yield curve has dis-inverted which is often the precursor to a recession. It is not a perfect indicator – nothing is – but the fact is we have arguably not had a normal economic cycle, whereby rising interest rates slows activity to quell inflation, for 25 years. It should not be a surprise if that’s what transpires in the coming months.

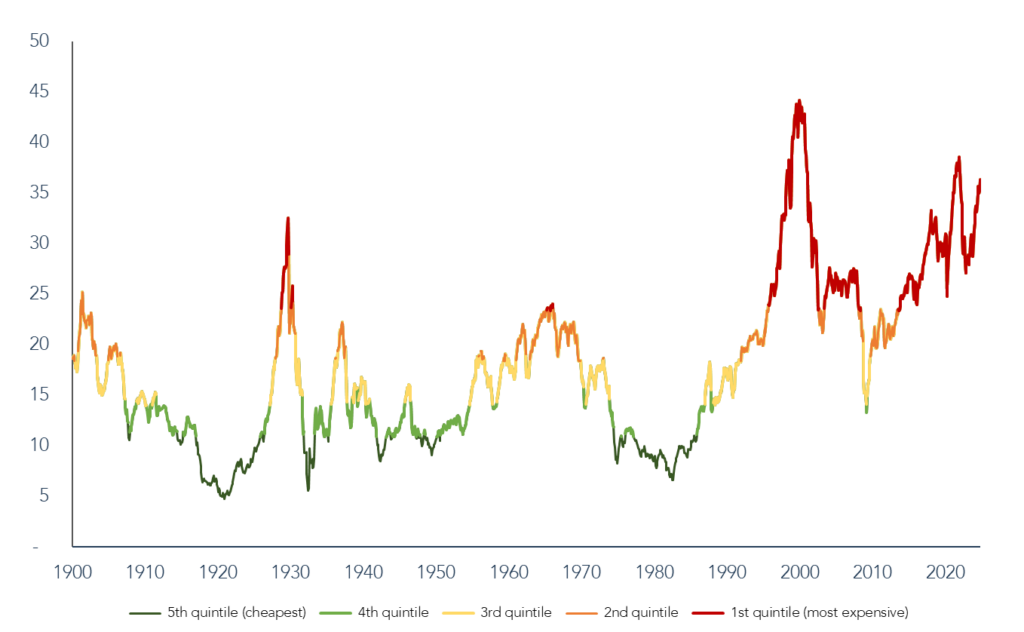

As regards to equity market valuation, this can be shown in absolute as well as relative terms. In absolute terms we can cite long-term measures such as the US CAPE, which currently stands at 36.7x representing one of the most elevated points in history.

Figure 1 – US Cyclically Adjusted Price/Earnings ratio (US CAPE)

Source: Robert Shiller, Yale University,31 October 2024. Past performance is not a guide to future performance. The CAPE Ratio (also known as the Shiller P/E or PE 10 Ratio) is an acronym for the Cyclically-Adjusted Price-to-Earnings Ratio. The ratio is calculated by dividing a company’s stock price by the Average of the company’s earnings for the last ten years, adjusted for inflation. All references to benchmarks are for comparison purposes only.*10 year average annualised total return based on CAPE valuation shown in left hand chart.

In relative terms, equities look stretched relative to fixed income. It has been our contention for some time that the fixed income market has made a major readjustment to the change in the economic landscape but that the equity market has yet to. It is remarkable that for the first time in 22 years the yield on bonds is now greater than the earnings yield offered by equities in the US.

Figure 2 – US Equity Earnings Yield Premium to Fed Funds Rate

Source: Bloomberg, 31 October 2024. Past performance is not a guide to future performance. Earnings yield is the 12-month earnings divided by the share price. Earnings yield is the inverse of the P/E ratio. Earnings yield is one indication of value; a low ratio may indicate an overvalued stock, or a high value may indicate an undervalued stock.

That the material change in the cost of capital has yet to impact equity valuations is notable but not necessarily surprising given the usual lag between changes in interest rates and the effect on the economy and employment. But as conservative investors with an eye to the downside, we believe this is an environment that demands a cautious approach. The time for taking more risk will be when valuations afford us greater opportunity for returns as well as more protection from material losses.

Notwithstanding this broader point, idiosyncratic opportunities may of course arise. Two such opportunities have been Amadeus IT (‘Amadeus’) and Rentokil Initial (‘Rentokil’) which have recently been added to the Trust.

Amadeus

Amadeus is a leading global technology provider for the travel industry based in Spain offering critical IT services to airlines, travel agencies, and hospitality businesses. The company’s main business areas are Air Distribution, Airline IT, and Hospitality IT, with each contributing to its revenue and growth strategy. Despite facing some disruption in its distribution business, Amadeus continues to show resilience and adaptability, positioning itself well for future growth.

Amadeus’s Air Distribution business, which includes its Global Distribution System (GDS), connects travel agents and airlines, facilitating flight bookings. Before the internet transformed the industry, GDS networks were crucial for connecting travel agents to airlines, offering a central platform for booking flights. In the pre-internet era, GDS networks were the only way to access airline inventory in real-time. However, with the rise of online booking platforms and direct airline websites, GDS systems have become less critical. GDS networks today accounts for about 30% of air travel bookings.

There is increasing speculation that GDS networks might be under threat due to the introduction of New Distribution Capability (NDC) by the International Air Transport Association (IATA). NDC is a new technical standard that allows airlines to offer more customized products. This has led to concerns about disintermediation of GDS networks, which are based on older technology. Additionally, NDC theoretically makes it easier for airlines and travel agencies to connect directly, potentially reducing the need for GDS.

While NDC poses a challenge, Amadeus is well-positioned to weather the storm. It holds a 45% market share in the GDS space and has been gaining ground, outperforming competitors like Sabre. Amadeus is investing heavily in its NDC capabilities to stay relevant and has fully embraced the new technical standard. It has proven that it can adapt and innovate, and the overall impact of NDC will likely be limited to specific high-volume markets like North America.

The GDS travel distribution network has been built through the decades, with a carefully designed incentive structure to ensure that every stakeholder finds the network valuable. Ripping up the current ecosystem might be attractive in theory, but hard to do in practice. American Airlines tried to move volumes aggressively away from GDS networks in 2023, only to have to reverse this move in 2024 as it was losing businesses to its competitors. While the transition to NDC will need to be managed carefully, we believe Air Distribution will remain a slow growing but stable business for Amadeus.

With the market heavily focused on the Air Distribution business, investors appear to be overlooking the long-term growth potential of the two other divisions, which collectively already account for nearly 60% of profits.

Amadeus’s Airline IT segment has been a consistent driver of growth, compounding sales at 19% per year leading up to Covid. Half of airline passengers in the world (excluding China) interact with Amadeus’s Passenger Service Systems (PSS) software when buying tickets and checking-in for their flights. PSS systems are sold to airlines, across both full-service carriers and low-cost airlines, and play a critical role in streamlining their day-to-day operations while enhancing the overall passenger experience. The technical superiority of Amadeus’s solutions has enabled it to gain significant market share at the expense of competitors, and the company continues to win major contracts with airlines.

The IATA ONE Order initiative, which aims to simplify the airline booking process, will give Amadeus the opportunity to expand its share of wallet, opening up new sales opportunities. The company has developed a leading product to respond to the changing Airline IT landscape called Nevio. The company has already signed up three new customers for Nevio, including British Airways.

Finally, Amadeus’s Hospitality IT division is emerging as another strong growth engine, contributing 16% of sales and 10% of profits. The company is applying the same strategy that made it a leader in Airline IT to the hospitality sector. Amadeus’s Central Reservations System (CRS) is used by major hotel chains like IHG and Marriott, enabling hotels to manage bookings more efficiently and provide customized pricing options.

The hospitality market remains underpenetrated when it comes to IT solutions, presenting a significant growth opportunity for Amadeus. The company is well-positioned to capitalize on this, leveraging its scale and expertise from the airline sector. As more hotels adopt IT solutions, Amadeus’s hospitality business is expected to continue growing at double-digit rates.

A distinguishing feature of Amadeus, and what gives us comfort in the long-term prospects of the business despite short-term disruption fears, is its long-standing commitment to R&D. The company spends around €1bn annually in R&D, or around 20% of sales. Whether it’s advancing NDC capabilities, developing new airline IT solutions like Nevio, or expanding its hospitality IT offerings, Amadeus has a history of anticipating the future needs of its customers and delivering innovative solutions. Amadeus has also made some smart acquisitions in the past to cement its leadership position, such as the acquisition of Navitaire, the leading PSS provider to the low-cost industry.

Putting it all together, we believe Amadeus can grow sales at a healthy high-single-digit rate for the foreseeable future, with profit growing at a faster rate as the company completes its transition to the cloud. The company has attractive profitability, with a net income margin of 20%. Being a software business, organic growth does not require any significant capital investments. This attractive growth profile is available at an attractive 5.3% FCF yield.

Rentokil

We are equally excited by the opportunity that has appeared in Rentokil. Some will remember this business from when it was managed by Clive Thompson in the 1980s and 1990s. It was a great example of a business that became a conglomerate via acquisition which was fashionable at that time. It was successful for a period – so successful that Mr Thompson gained the nickname “Mr 20%” in reference to the earnings per share growth – but like so many of these situations ended badly. The shares ultimately went on to lose 92% from the then peak in 1998 to 2009.

Today it is a very different and much better business. Much better than investors appreciate in our view. Under the stewardship of Andy Ransom, Rentokil has refound its feet. It is now much more focussed on commercial and residential pest control leading it to becoming the global leader with the broadest geographic coverage, including being the largest player in the lucrative US market. It also has smaller businesses engaged in facilities management, providing plants and workwear.

Pest control is an inherently attractive industry (at least from an investment standpoint) given the resilient, repeat, non-discretionary nature of spending in this category, often mandated by regulation, leading to high recurring revenue. The industry is likely to grow faster than the broader economy as populations urbanise and greater wealth leads to less tolerance for pests. Longer term a warming planet may further increase the need for Rentokil’s services. Companies in this industry are therefore operating in a structurally favourable environment, and the industry is fragmented so this underlying growth can be enhanced via acquisition.

In addition to these industry attractions, companies in the sector enjoy durable competitive advantages from scale. Greater scale leads to a superior cost position to the benefit of margins and returns. The ability to deploy capital in size also gives an edge to businesses when making acquisitions. They are also well placed to invest in technology and innovation. Familiarity from size also burnishes brand equity.

Pest control (and facilities management) is a ‘global but local’ and ‘route based’ business that relies on many small local branches. High market share leads to density, which in turn leads to higher margins by enhancing productivity and reducing costs. This makes for a tough competitive environment for smaller operators and correspondingly attractive margins and sustainable returns for dominant companies like Rentokil.

For all these reasons companies in this sector have enjoyed a material uplift in valuation over the last decade or so as well as substantial private equity interest. The number 2 player in the US, Rollins (which admittedly is purely focussed on pest control in one geography), enjoys a price/earnings multiple of 52x. Conversely Rentokil trades on a much more conservative c.17x 2024 EPS with a 2.3% dividend yield. So why such a big discount?

In a bold move the company announced in December 2021 that they would be acquiring a company called Terminix using a combination of shares and cash for $6.7bn (compared to Rentokil’s market capitalisation at the time of £9.5bn). This was the number 2 pest business in the US (behind Rollins but ahead of Rentokil). The deal catapulted Rentokil into being the clear leader in the US with a 30% market share relative to Rollins at c.20% as well as the global leader. It also skewed Rentokil’s revenues to the US (c.61% of total revenue), as well as to pest control (c.75% of total revenue). This was a strategically decisive deal.

At STS Global Income & Growth Trust we are generally wary of large corporate M&A, and this was no exception. Indeed, the announcement made us wary before committing any capital to the business. This proved to be the correct decision as the company, perhaps inevitably, struggled with the integration of Terminix. This led to a material decline in the share price and a corresponding fall in earnings expectations among investors.

Therein lies the opportunity to establish an investment in a high-quality global asset at a tantalising valuation. We are not the only ones that see this opportunity. Nelson Peltz of Trian Partners, an activist investor for whom we have a lot of respect and alongside whom we have invested successfully in the past, has taken a stake and has a representative on the Board. Given the main issue here is one of execution we think Trian may be a steady hand on the tiller as they have been in companies such as Unilever and Procter and Gamble in recent operational turnarounds.

Overall, we believe we have invested in a company with identifiable and sustainable competitive advantages in an attractive and growing industry that trades at a low valuation for a clearly identifiable reason which we believe will resolve to the market’s satisfaction in time. If it is the job of a quality income manager to invest in good businesses when they are out of favour, this is a textbook example.

Coda: Trumpland

The US election result demands comment. As the Economist put it, we are now living in Trumpland. The emphatic victory with a clean sweep of the presidency, the Senate, and the House of Representatives, combined with a like-minded Supreme Court gives the President-Elect largely unchecked power. Commentary from the US media and the reaction in global markets has been fulsome and in some ways with good reason. Short term market moves have been consistent with a generally upbeat attitude in capital markets as investors begin to price in the perceived benefits of the Trump agenda. Hence, we have seen strength in equity markets in areas such as banking, technology, Bitcoin and European defence. The US dollar has been strong, spreads tight and equity volatility has declined.

At the same time less favoured areas have struggled, most obviously renewable energy and non-US currencies including Sterling but most impactfully perhaps the US bond market. The US 2-year note has climbed from a recent low of 3.54% to 4.26%, similarly the US 10-year 3.64% to 4.43% as the Treasury market correctly anticipated a Trump win. These are big moves and indicate the less economically (and possibly societally) attractive parts of the agenda. The enactment of unfunded tax cuts, harsher treatment of migrants and especially the imposition of tariffs are all likely to be inflationary. When this is combined with a greater questioning of the independence of the US Federal Reserve, a more balanced view than is implied by recent excitement may be wise. It is notable to us that BCA, one of our research providers, have increased the likelihood of a recession in the US in the coming months because of these measures.

Of course, like so much associated with The Donald we don’t really know what will happen and how much of the rhetoric will translate into policy. But we must be careful before leaping to conclusions especially in the context of elevated sentiment and valuations. If the core tenets of his approach are tax cuts, tariff increases, deregulation, larger fiscal deficits and slower working age population growth, then they represent a mixed bag at best and potentially both inflationary and recessionary. The good Donald has been priced in, the bad Donald not, which leaves markets vulnerable to disappointment.

Run straight

We remain focused on allocating capital to high quality global income franchises. At the same time, we remain patient and disciplined, determined not to overpay. With markets priced for perfection, opportunities to score may be relatively rare but they can and do arise and we will not deviate from the line when they appear.

Please refer to Troy’s Glossary of Investment terms here. Performance data relating to the NAV is calculated net of fees with income reinvested unless stated otherwise. Past performance is not a guide to future performance. Overseas investments may be affected by movements in currency exchange rates. The value of an investment and any income from it may fall as well as rise and investors may get back less than they invested. The historic yield reflects distributions declared over the past twelve months as a percentage of the Trust’s price, as at the date shown. It does not include any preliminary charge and investors may be subject to tax on their distributions. Tax legislation and the levels of relief from taxation can change at any time. The yield is not guaranteed and will fluctuate. There is no guarantee that the objective of the investments will be met. Investment trusts may borrow money in order to make further investments. This is known as “gearing”. The effect of gearing can enhance returns to shareholders in rising markets but will have the opposite effect on returns in falling markets. Shares in an Investment Trust are listed on the London Stock Exchange and their price is affected by supply and demand. This means that the share price may be different from the NAV.

Neither the views nor the information contained within this document constitute investment advice or an offer to invest or to provide discretionary investment management services and should not be used as the basis of any investment decision. Any decision to invest should be based on information contained within the Investor disclosure document the relevant key information document and the latest report and accounts. The investment policy and process of the Trust(s) may not be suitable for all investors. If you are in doubt about whether the Trust(s) is/are suitable for you, please contact a professional adviser. References to specific securities are included for the purposes of illustration only and should not be construed as a recommendation to buy or sell these securities. Although Troy Asset Management Limited considers the information included in this document to be reliable, no warranty is given as to its accuracy or completeness. The opinions expressed are expressed at the date of this document and, whilst the opinions stated are honestly held, they are not guarantees and should not be relied upon and may be subject to change without notice. Third party data is provided without warranty or liability and may belong to a third party. Ratings from independent rating agencies should not be taken as a recommendation.

Please note that the STS Global Income and Growth Trust is registered for distribution to the public in the UK and to Professional investors only in Ireland.

Issued by Troy Asset Management Limited (registered in England & Wales No. 3930846). Registered office: 33 Davies Street, London W1K 4BP . Authorised and regulated by the Financial Conduct Authority (FRN: 195764) and registered with the U.S. Securities and Exchange Commission (“SEC”) as an Investment Adviser (CRD: 319174). Registration with the SEC does not imply a certain level of skill or training.

© Troy Asset Management Limited 2024.